Global markets remained remarkably composed on Wednesday as investors awaited the U.S. Fed Rate Decision and assessed escalating geopolitical risks in the Middle East. While concerns around inflation and regional conflict persisted, equity indices, bond yields, and commodities reflected measured investor sentiment. Market participants are increasingly signaling confidence in the Fed’s data-driven strategy and resilience in global financial systems.

This report explores how steady market behavior amid uncertainty underscores a shift in investor psychology, from fear-driven reactions to a focus on long-term fundamentals, monetary policy expectations, and global economic signals.

Heightened Geopolitical Risk Rattles Markets

Reuters reports that financial markets moved cautiously on Wednesday, with investors hesitating to make bold moves amid heightened Middle East tensions and anticipation surrounding the U.S. Federal Reserve’s upcoming interest rate decision. Ongoing conflict between Israel and Iran, now in its sixth day, and President Donald Trump’s increasingly aggressive rhetoric kept risk appetite subdued across equities, commodities, and currencies.

Local media reported that thousands of Tehran residents have fled due to escalating strikes, particularly those targeting Ayatollah Ali Khamenei’s inner circle. As uncertainty mounted, oil prices surged earlier in the week, amplifying concerns over inflation, already strained by U.S. tariff threats on major trading partners.

European indices saw minimal movement, with the STOXX 600 flat, while the FTSE 100 and Germany’s DAX inched up by 0.2%. Brent crude fell to $75.92 a barrel, despite broader concerns about potential supply disruptions in the Strait of Hormuz, a vital oil shipping route.

Moreover, reports of evacuations in Tehran and Israeli strikes targeting Iranian leadership figures added to global unease. The U.S. expanded its military presence in the region following former President Trump’s call for Iran’s unconditional surrender, prompting speculation about a broader U.S. intervention.

Fed Decision Looms Amid Weak U.S. Data and Rate Speculation

Market focus now turns to the Federal Reserve’s upcoming interest rate decision. While no immediate rate changes are expected, attention will be on the central bank’s economic forecasts and the updated “dot plot” for clues on the trajectory of monetary policy.

Recent U.S. data showed retail sales fell 0.9% in May, the sharpest decline in four months, raising concerns about consumer demand. Yet inflation has remained relatively stable, complicating the Fed’s path. Harvey Bradley of Insight Investment noted that while the Fed may reduce the number of expected rate cuts due to geopolitical risks and rising oil prices, weakening labor market signals could still justify easing.

Meanwhile, rate traders have amassed record futures positions betting that Trump’s potential Fed appointee in 2026 will push for immediate rate cuts. This trade, which surged in volume earlier in the week, reflects growing speculation that the Fed’s post-Powell direction could turn more dovish under a new administration.

Mixed Market Reactions Across Assets as Uncertainty Prevails

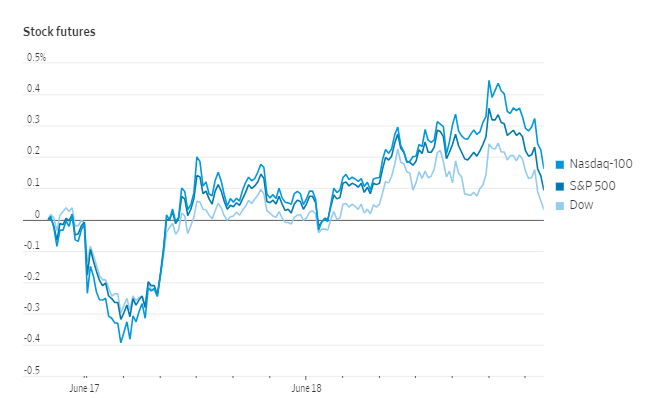

Stock and commodity markets presented a mixed picture globally. In the U.S., futures for the S&P 500, Nasdaq, and Dow Jones showed modest gains after Tuesday’s decline. Asian markets ended unevenly, with Japan’s Nikkei up 0.9%, helped by Nintendo’s strong performance, while Hong Kong’s Hang Seng slid 1.3%. European shares saw minimal changes, with France’s CAC 40 and the FTSE 100 up 0.1%, and the Stoxx 600 down slightly.

Gold prices traded within a narrow range at $3,386 an ounce, reflecting investor caution. U.S. Treasury yields were largely steady, with the 10-year yield inching up to 4.4027% and the two-year yield at 3.9586%. The dollar weakened slightly, and Bitcoin edged 0.4% higher after the Senate passed stablecoin regulation, marking a key development in crypto oversight.

Amid these moves, broader concerns linger over rising energy prices, Trump’s unresolved trade disputes, especially a July 9 tariff deadline, and the potential for more aggressive foreign policy actions. As the Federal Reserve prepares to deliver its decision, markets remain highly sensitive to both economic signals and geopolitical developments.